Medicare (Once And) For All

Medicare (Once And) For All

Setting the record straight on single-payer

I had such high hopes for us.

When the Medicare For All debate started to gain traction, there was a lot of outrage. The bulk of it, I assumed, stemmed from a lack of clarity on how exactly Medicare For All or a single-payer system works. It’s understandable: it’s not a format we’re used to in the United States, and as our ongoing refusal to adopt the metric system suggests, we don’t like being late to the party. Still, I figured the uproar would subside the more people learned about the policy. Has it? Well, yes and no.

A Reuters-Ipsos poll in August 2018 found that 70% of Americans (including 52% of Republicans) support Medicare For All. However, that number drops to 38% when it’s made clear that Medicare For All would be mandatory (for all). Some of that decline is attributable to the the right-wing talking point of “Medicare For All = SOCIALISM,” some is due to people’s unwillingness to give up their “freedom” (read: private insurance); the rest is a potpourri of various gripes and grievances. All of it, however, can be traced back to the fact that most people still don’t fully understand Medicare For All.

I (wise, a genius) have waited long enough for you people (fools, scoundrels) to catch up. Here are the most common questions about/objections to Medicare For All, along with my helpful responses.

“What is Medicare For All?”

We’ll start with an easy one. In short, it is one single insurance plan for every American that would be 100% free at point of care (and after): no copays, no deductibles, no coinsurance. It would cover everything your private insurance already covers: hospital services, inpatient and outpatient care, ambulatory patient services, primary and preventive care, prescription drugs, medical devices, mental health & substance abuse treatment, lab/diagnostic services, pediatrics, dental, vision, audiology, and reproductive care (maternity, newborn care, and, yes, abortions).

“Medicare For All is socialized medicine!”

“Socialized medicine” refers to a government-funded healthcare system; that is, providers are government employees and hospitals are government-owned. Government employees are seen as wasteful and inefficient – precisely the kind of person you don’t want to entrust with your care. Medicare For All is a single-payer system, not socialized medicine.

“What is ‘single-payer’?”

Exactly what it sounds like.

Our current system is a “multi-payer” system with a ton of different public and private insurers: Blue Cross/Blue Shield pays Person A’s medical bills, Aetna pays Person B’s, Anthem pays Person C’s, Cigna pays Person D’s, and so on. Each person’s plan varies in terms of coverage and cost, and private insurers can refuse coverage if your health history indicates you’re going to cost them more money than they’ll make from you in premiums. A single-payer system means that everybody’s medical bills would be paid from one source (the government) and that everyone has coverage.

“I don’t trust the government to handle my health care!”

When you get sick, your health insurance company doesn’t send out an adjuster to do a physical, right? No, you just…go to the doctor. The process for getting care wouldn’t change under Medicare For All – the government wouldn’t “handle” your health care any more than your private insurer does now.

When it comes to our insurance, we really only care about two questions: “Does my policy cover this?” and “How much will it cost?” Under our current system, the answers are “Maybe” and “Depends on the first one”; under Medicare For All, the answers would be “Yes” and “Nothing (if it’s medically necessary).”

“Obama said ‘You can keep your doctor’ and then I couldn’t!”

Yeah, Obama fucked that one up.

The Affordable Care Act was a huge step forward in that it provided health coverage to more than 20 million Americans who previously couldn’t get it elsewhere. (The ACA made it illegal for private insurers to turn someone down because of a pre-existing condition.) But there are problems with Obamacare, the biggest being that it still has to compete with private insurers, which is a fight that a government-funded insurer can’t win. The only way it can win is by removing the competition.

I’ll explain.

Let’s say a provider has to perform a 30-minute physical. The Medicare rate – the minimum rate – is $50 for that physical, meaning the provider can bill $50 to the government for performing it and the government will pay it. For private insurers, that $50 is the starting point, but there’s no maximum rate for that physical. Obviously, no private insurance company is going to pay each doctor $1 million for a physical, so there’s a theoretical limit, but private insurers can – and do – pay doctors more for the same work. A recent study by RAND found that private insurers pay anywhere from 150% to 400% of the Medicare rate for providers’ work.

This is where Obama over-promised. If doctors – either in a private practice or as part of a hospital group – have the choice of getting paid the Medicare rate of $50 or the private insurer rate of $200 for the same work, most will take the $200. In some cases, when the ACA took effect, doctors decided to stop seeing anyone whose insurance didn’t pay that $200, including their own existing patients. As a result, people whose insurance only paid $50 suddenly found that their doctor no longer took that insurance. It’s not entirely the doctors’ fault: whether they run their own practice or work for a big hospital group, all providers are under pressure to maximize the amount of billable work they do in a given day. (This system brought to you by Capitalism™: “Bleed ‘em dry and let ‘em die!”)

Point is, private insurers will always be able to pay more than the government, which is why the ACA – while still tremendously helpful – hasn’t solved a lot of the underlying problems in the American healthcare system. Under Medicare For All, the government would no longer have to compete with private insurers, and your doctor would either have to: 1) take the government rate, 2) practice on a cash-only basis, or 3) quit. So while it’s technically possible that your doctor might say “Screw it” and switch to cash only or retire, for the vast majority of us, everything would stay the same.

Also, if your doctor is willing to prioritize maximizing their profits over taking care of their patients, your doctor is a dick and you’re better off finding a new one.

“Medicare doesn’t cover _______!”

Correct – there are a lot of gaps in existing Medicare and/or Medicaid coverage. Under Medicare For All, Medicare would be reworked to cover all the things listed above (primary/preventive care, mental health care, reproductive care, hearing/dental/vision care, and so on). All the different components of Medicare (Part A, Part B, Part C, Part D, etc.) would be consolidated and expanded under one large Medicare umbrella.

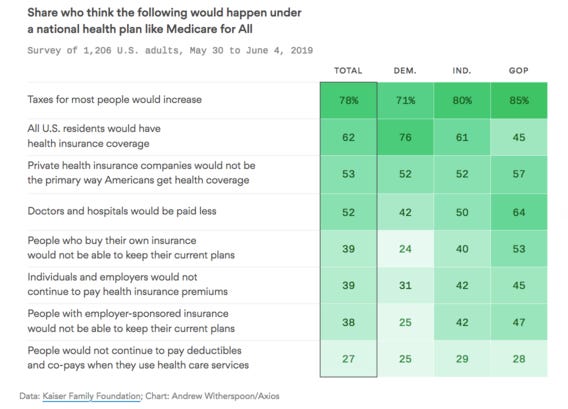

“My taxes would go up!”

Again, correct – taxes would increase in order to offset the cost of Medicare For All. Sanders recently released a white paper laying out the different options, the most likely of which seems to be a 4% “income-based premium” for households making over $29,000 a year.

So let’s say your household makes $50,000. You’d pay a 4% premium ($2,000) per year (actually less after your standard deduction, but I’m not doing tax math). That sounds like a lot…until you remember that under the existing system, the average household making $50,000/year already pays 5% of its income towards health care coverage alone, not including out-of-pocket expenses like copays and deductibles; when you factor in all the out-of-pocket costs, that percentage jumps to 7.9%.

So yes, you’d pay more in taxes. But the tax increase would be offset – if not in full, then at least partially – by removing that premium cost for private coverage, and you’d save money on copays and deductibles, since anything covered under Medicare For All (see above) would be 100% free at the point of care. Plus, you wouldn’t have to worry about getting a bill 3 months after a doctor visit telling you actually, we don’t cover ear exams, you owe us $1,742.94, please call us immediately to schedule your payment or we’ll make your life a living hell.

“They’ll start rationing care like they do in Canada, that’s why they come here for surgery!”

I have some alarming news. Healthcare in America is already rationed: if someone can’t pay for a doctor, they don’t see one.

In 2016, an estimated 63,459 Canadians traveled outside Canada to receive medical treatment. In 2017, an estimated 1.4 million Americans left the United States to receive medical treatment. Are there longer wait times for non-emergency surgeries in Canada? Yes – the average wait time is about 10 weeks. Part of that is because Canada has less hospital space than the United States (there are 516 citizens for every hospital bed in Canada; there are only 353 people per bed in the United States). But the “average” Canadian isn’t coming to the U.S. for their surgeries because our system is so much better – they’re coming here because they have money and can afford to spend it in order to cut the line.

Even if you think Canada’s wait times are unacceptable, it’s not necessarily a given that Medicare For All would have the same effect here; again, we have more hospitals and more beds, and the average hospital stay in the U.S. is about 2 days shorter than in Canada (4.6 days and 6.8 days, respectively). Besides, do you really think waiting a few extra weeks for a non-emergency surgery is so terrible a fate that it’s worth sacrificing the lives of the thousands of people who can’t afford healthcare?

“I work hard for my insurance. This just incentivizes people to be lazy!”

First of all, no you don’t. You work hard for money, just like everyone else does. And nobody’s going to find themselves on Easy Street just because they don’t have to worry about dying from the flu.

Nevertheless, a KPMG study found that an increase in government spending on a universal healthcare program correlates to an increase in national economic activity. Why? Because a healthy workforce is more productive.

“We can’t afford it!”

Various studies have attempted to calculate the cost of Medicare For All, and while there’s no consensus on an exact figure, the ballpark range is $28-$32 trillion over the next 10 years; Bernie Sanders himself estimates that it could cost up to $40 trillion over 10 years. And sure, that seems like a lot.

In 2017, Americans spent $3.5 trillion on healthcare. Using Sanders’ $40 trillion estimate, Medicare For All would cost about $5 trillion more over the next 10 years, right? Well, no. According to the Centers for Medicare & Medicaid Services (CMS), healthcare costs are projected to grow by an average rate of 5.5% per year.

Let’s say we implemented Medicare For All on the first day of 2021. At the end of the 10 year period, on January 1, 2031, we’ll have spent $40 trillion on Medicare For All. According to CMS projections, if we keep our existing system, we’ll have spent $56.2 trillion in that same time period. Of course, people seem to only bring up the we can’t afford it argument when it’s about something they don’t like, but just in case someone is actually concerned with cost, well, there you go.

And while the cost of our existing system keeps going up, Medicare For All’s costs would…go down. Look at that, a segue opportunity.

“We’ll go broke paying for everyone’s healthcare forever!”

Here’s the thing. Under our current system, everybody technically has “access” to healthcare; that is, if things get bad enough, they can go to an ER. Once they’re stabilized, I believe there’s some sort of trap door or network of slides to transport them directly to bankruptcy court. (Also, any time you hear a politician use the phrase “access to healthcare,” you can safely interpret it as “I’m not going to change anything.”)

Be honest: even if you have insurance, you still avoid going to the ER if at all possible. Why? Because even with great health insurance, ER visits are expensive as hell. The copay for your primary care doctor is $20; for urgent care it’s $50; for the ER, it’s probably at least $100. And it’s not just the copay that goes up, it’s the cost of the services themselves: according to a 2013 NIH study, the average ER bill is $1,233. The average cost of an initial visit with a primary care provider, on the other hand, is $100-200. Why? Because the earlier a health issue is caught, the easier (and cheaper) it is to treat.

Here’s an example.

Let’s say you don’t have insurance. You haven’t been to a doctor in a few years, and lately you’ve been having sporadic irregular heartbeats or frequent headaches. Everybody gets headaches, though, so you just take some Advil and keep going. A few months later, you go for a run, but soon after you start you begin to feel really fatigued: your heart is pounding, and you feel like you can’t catch your breath. You cut your run short, head home and rest; pretty soon you start to feel better, so you tell yourself it was just a weird, one-off occurrence. You don’t see a doctor.

A few more months pass. One day you’re carrying groceries up the steps to your apartment and the feeling hits again: fatigue, shortness of breath, dizziness, all of it. This time, you’re worried enough to make an appointment with your old doctor. They refer you to a cardiologist – depending on how much cash you have, you may or may not make the appointment with the specialist right away. But let’s say you just got your tax return, so for right now money’s not an issue.

You schedule the cardiologist appointment for the following week, and that’s when you find out that you have Stage 3 congestive heart failure.

If you’d had insurance, your doctor probably would’ve diagnosed you with hypertension 3 years ago. If you’d had insurance, your doctor could have suggested dietary/lifestyle changes and prescribed heart medication 2 years ago when you had Stage 1 CHF. Or last year when it progressed to Stage 2. At Stage 3, without a transplant, there’s no going back to a normal life. Even everyday activities will become more difficult. By the time you reach Stage 4, the symptoms are present all the time, even when you’re just lying in bed. All they can do is make you comfortable.

“Well, I have insurance so this isn’t my problem.”

Wanna bet? The scenario I described above doesn’t just apply to uninsured people – it also applies to people who do have insurance but have high deductibles they can’t pay. It applies to people whose plan doesn’t cover certain services (which is the same as not having insurance at all). It applies to people who had insurance, then lost it when they got laid off and died taking antiquated medicine because they could no longer afford the cost of their insulin.

This system forces people with chronic health conditions to drag themselves to work every day, because keeping their job is literally a matter of life or death. You may have insurance today, but what happens if you have a terrible accident or develop a crippling illness that keeps you out of work for so long that your company has no choice but to replace you? If you think it can’t happen to you, that’s only because it hasn’t yet.

People don’t avoid going to the doctor because they don’t care about their health. They avoid going to the doctor because they can’t afford to care about their health. Medicare For All would remove the financial barrier to care, which would allow providers to practice preventive medicine and identify/treat health issues before they become insurmountable problems. Not only is it more cost-effective than the system we have now, but people wouldn’t have to choose between dying prematurely from preventable or treatable diseases and paying their rent.

Ultimately, that’s what this debate boils down to: Is it worth letting tens of millions of lives wither and die on the vine so we can keep telling ourselves that the horrible system we have now is the best we can do?

If your answer is “no,” congratulations: you support Medicare For All.